Intertrust shows sound performance over 9M 2016

![]() GlobeNewswire •Nov 3, 2016, 1:16 AM

GlobeNewswire •Nov 3, 2016, 1:16 AM

Full Year 2016 adjusted net income per share including Elian on a proforma basis

of approximately €1.42 expected

Intertrust N.V. Q3 & 9M 2016 results

Amsterdam – November 3, 2016 – Intertrust N.V. (“Intertrust” or “the Company”) [ticker symbol INTER], the leading global provider of high-value trust and corporate services, today announces its results for the third quarter and the nine months ended September 30, 2016.

Presentation of financial and other information

Financials are presented on an adjusted basis, before specific items and one-off revenues/expenses. Year-to-date (YTD) financial information represents unaudited financial information for the nine months ended September 30, 2016. The acquisition of Elian was closed on September 23, 2016.

In € millions 9M 2016 9M 2015

Adjusted revenue 265.0 253.4

Adjusted EBITA 105.6 102.6

Adjusted EBITA Margin 39.9% 40.5%

Adjusted net income 77.7

Adjusted net income per share (€)* 0.88

Adjusted revenue of €265 million grew by 4.6%.

Adjusted EBITA of €105.6 million grew by 3%.

Adjusted EBITA margin of 39.9%. This is a 61bps decrease versus 9M 2015.

Note: Rounding differences may occur as calculations are based on nine month figures not rounded to millions.

* Adjusted Net Income per share calculated using weighted average number of shares outstanding as per September 30 (87,917,883), including issuance of shares for the acquisition of Elian

David de Buck, Chief Executive Officer of Intertrust, commented:

“We are generally satisfied with the overall performance of the group, the main exception being Cayman. Excluding Cayman, our Adjusted revenue on a constant currency and proforma basis grew 4.6% in Q3 and 5.3% for the 9M period.

Our third quarter revenue growth was negatively impacted by weaker-than-expected performance in Cayman, fewer available billable hours due to the continued tight recruitment market in Luxembourg and continued weakness in specialised services in The Netherlands. The underlying business remains strong with our sales pipeline being 8 percent higher than same period last year. One of the short-term effects of Brexit has been the delay of investment decisions due to uncertainty surrounding how Brexit will play out.

The Elian acquisition was closed on September 23 and the integration is in full swing. The new, post-merger management structure was announced and implemented. All but one of the office moves and the rebranding of Elian to Intertrust will be completed in the coming 6 weeks. Combined sales strategies for the newly adopted service lines have been finalised and are being implemented. We have received positive feedback from clients and business partners across the globe and cross-selling opportunities between the companies are already being realised. Synergy forecasts of £10.4 million remain unchanged. Per the period September 23 – September 30, 2016, Elian contributed €1.6 million in Adjusted Revenue and €0.6 million in Adjusted EBITA. We look to the coming year with confidence, and we are excited with the opportunities Elian brings us.”

Highlights Q3

On September 23, 2016 Intertrust completed its acquisition of Elian, the Jersey-based regional trust and corporate services provider for £435 million.

Interim dividend of €0.24 per share was announced, payable on November 30, 2016.

175,000 shares were repurchased in order to meet obligations under an employee share plan.

Adjusted financial information before specific items and one-off revenues/expenses. 2016 figures include CorpNordic acquisition

Adjusted Net Income per share is calculated as Quarterly or 9 Months Adjusted EBITA less net interest costs and less tax costs divided by the number of shares outstanding (85,221,614) before the additional issuance of shares for the acquisition of Elian. When using the weighted average number of shares outstanding as per September 30 (87,917,883), the Quarterly and 9 Months Adjusted Net Income per share would be €0.27 and €0.88 respectively

As of September 30, 2015 and September 30, 2016 respectively

Annualised numbers based on Adjusted revenue before specific items and one-off revenue/expenses.

Financial highlights Q3 2016 versus Q3 2015

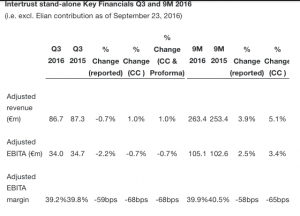

Adjusted revenue for the quarter decreased by 0.7% to €86.7 million (Q3 2015: €87.3 million). On a constant currency basis, Adjusted revenue grew by 1.0%. Revenue growth continues to be driven by the ARPE growth whilst the number of entities declined. The number of entities decreased mainly due to low ARPE structures exiting in Cayman due to the re-entry of a competitor into the market. Excluding the performance of Cayman, Adjusted revenue on a constant currency and proforma basis grew by 4.6% during the quarter.

In addition, revenue growth in Q3 2016 was impacted by the lower number of billable hours in Luxembourg due to fewer FTEs than budgeted and lower than budgeted specialised services in the Netherlands (combined revenue impact €2.6 million). Negative foreign exchange rate revenue impact was €1.5 million.

Adjusted EBITA for the quarter decreased by 2.2% to €34 million (Q3 2015: €34.7 million). On a constant currency basis, Adjusted EBITA decreased by 0.7%.

Adjusted EBITA margin was 39.2% versus 39.8% for Q3 2015, a decrease of 59bps mainly driven by the deteriorated performance of Cayman, increased IT costs due to new hires and increased IT investment and increased Group HQ costs including the LTIP costs.

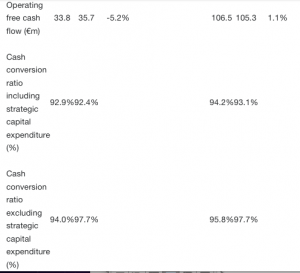

Total capital expenditure for the quarter was €2.5 million (Q3 2015: €2.8 million).

Q3 2016 cash conversion ratio excluding strategic capital expenditures was at 94% (Q3 2015: 97.7%).

Financial highlights 9M 2016 versus 9M 2015

Adjusted revenue in 9M 2016 increased by 3.9% to €263.4 million (9M 2015: €253.4 million). On a constant currency basis, Adjusted revenue grew by 5.1%. On a constant currency and proforma basis, i.e. including the contribution of CorpNordic for the first six months in 2015, Adjusted revenue grew by 2.6%. Revenue growth was particularly driven by strong performance of the Netherlands and Guernsey (albeit in GBP) and moderate growth in Luxembourg and in the ROW (also on proforma basis). The growth was negatively impacted by the loss in Cayman of certain low ARPE registered office business due to the re-entry of a competitor into the market. Excluding the performance of Cayman, Adjusted Revenue on a constant currency and proforma basis grew by a solid 5.3% over the 9M period.

In addition to the Cayman drag on revenue over the 9M period, the growth in revenue was impacted by a lower number of billable hours in Luxembourg due to fewer FTEs than budgeted stemming from a tight recruiting market and less capital markets-related services in the Netherlands due to market circumstances (combined revenue impact of €5.4 million) and foreign exchange rates (negative revenue impact of €2.9 million).

Adjusted EBITA over 9M 2016 increased by 2.5% to €105.1 million (9M 2015: €102.6 million). On a constant currency basis, Adjusted EBITA increased by 3.4%. Including the proforma contribution of CorpNordic for the first half year in 2015, Adjusted EBITA grew by 2.1%. EBITA growth was restricted by circa €4.5 million because of the reasons mentioned above including approximately €1.0 million of foreign exchange rate impact. Excluding the performance of Cayman, Adjusted EBITA grew by 7.2%.

Adjusted EBITA margin was 39.9% versus 40.5% for 9M 2015, a reduction of 57.8bps, partially driven by the consolidation of the lower margin CorpNordic acquisition. Including the proforma contribution of CorpNordic for the first six months in 2015, the EBITA margin decreased slightly by 21.7bps versus 9M 2015 mainly driven by increased IT costs due to new hires, increased IT investment and increased Group HQ costs including the LTIP costs.

Total capital expenditure for 9M 2016 was €6.5 million (9M 2015: €7.4 million), €1.8 million (9M 2015 €4.9 million) of which represented one-off strategic capital expenditure resulting from the implementation of the Business Application Roadmap, a company-wide standard software application platform. Increase in maintenance capex of €2.1 million in 9M 2016 versus 9M 2015 was mainly driven by IT related investments (IT hardware replacement and software development, the implementation of the outsourcing of datacentres of Intertrust, procurement of software) and some leasehold improvements.

9M 2016 cash conversion ratio excluding strategic capital expenditures decreased to 95.8% (9M 2015: 97.7%) mainly driven by the increase in maintenance capex.

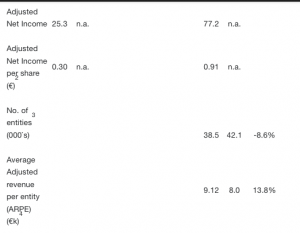

YTD annualised Average Revenue per Entity (ARPE) increased by 13.8% to €9.1 k (9M 2015: €8.0 k). Intertrust continues to see increasing hours per entity due to more complex structures, regulatory reporting requirements and focus on higher value-added entities. In addition, increased ARPE was partially driven by the outflow of lower-valued registered office entities in Cayman.

As of 9M 2016, Intertrust had 38,493 entities, a net outflow of 3,635 entities over the last twelve months mainly due to the re-entry of a competitor in Cayman (2,898 entities lost of which 1,554 in 2016) and one-time administrative adjustments of 170 entities in Netherlands and 276 in Guernsey.

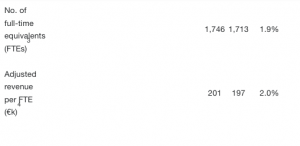

A net increase of 33 FTEs over the last 12 month period ended September 2016 was primarily due to the increase in billable FTEs (29 FTEs) mainly in the Netherlands and Luxembourg to support business growth. Intertrust maintained a billable versus total FTE ratio of 75%.

YTD annualised Adjusted revenue per FTE increased by 2% to €201 k (9M 2015: €197 k).

Adjusted net income and Adjusted net income per share

Adjusted net income Intertrust stand-alone for 9M 2016 was €77.2 million.

Adjusted net income per share for 9M 2016 on a stand-alone basis was €0.91 based on the number of shares outstanding excluding the Elian-related share issue.

Outlook

On a proforma basis including Elian for the full year and based on the actual number of shares at the end of Q3 2016 the Adjusted net income per share will be approximately €1.42.

Cayman is expected to continue to be negatively impacted by the re-entry of a competitor into the market for the rest of 2016 and modestly throughout 2017, after which we expect the business to stabilise.

For the medium term, objective reiterated of organic revenue growth slightly above market growth of 5% (estimated market CAGR for CY 2015 – 2018E).

Adjusted EBITA margin improvement objective including Elian is reiterated at 300-350bps by CY 2018E over the Intertrust stand-alone CY 2015 proforma Adjusted EBITA margin of 40.4%.

Compared to the stand-alone guidance, interest costs for the combined company for the full year 2016, including new debt for the Elian acquisition, are expected to be approximately €21 million of which €4.0 million is related to the amortisation of financing fees (non-cash).

Cash conversion to continue to be in line with historical rates.

Maintenance / normalised capex will be 2 – 2.5% of revenues for the combined company.

Effective tax rates based on adjusted net income before tax will be approximately 16% after completion of the Elian acquisition (18% on a stand-alone basis). For 2016, we expect an effective tax rate slightly below 16%.

Unchanged target steady-state net debt to EBITDA ratios are at 2 – 2.5 times, with a temporary increase in the event of an acquisition.

Dividend policy is a target dividend of 40-50% of Adjusted net income. The first interim dividend of €0.24 will be paid on November 30, 2016 over the year ending December 31, 2016.

Performance in key jurisdictions

The Netherlands

Q3 Q3 % Change 9M 9M % Change

2016 2015 (reported) 2016 2015 (reported)

Adjusted revenue (€m) 29.7 28.5 4.5% 88.1 83.4 5.5%

Number of entities (000`s) 4.3 4.5 -3.8%

Annualised ARPE (€k) 27.2 24.8 9.7%

1. Adjusted financials before specific items and one-off revenues/expenses

In the Netherlands YTD 2016, Intertrust achieved year-on-year adjusted revenue growth of 5.5%, driven by continuing international investments and increased billable work force. Inflow of new entities YTD 2016 was in line with inflow over same period 2015. Inflow in Q3 2016 was higher than in Q2 2016 and at the same level as Q3 2015. A significant part of YTD outflow (approximately 170 entities) was related to a one-time administrative correction of a group of capital markets entities which were terminated before 2016. The correction had no revenue impact. Outflow in Q3 was in line with Q2 2016, predominantly reflecting end of life of client structures. ARPE growth continues as a result of transaction complexity and regulatory requirements demanding value-added services.

Luxembourg

Q3 Q3 % Change 9M 9M % Change

2016 2015 (reported) 2016 2015 (reported)

Adjusted revenue (€m) 18.9 18.5 2.2% 57.4 55.4 3.7%

Number of entities (000`s) 2.6 2.7 -2.7%

Annualised ARPE (€k) 29.5 27.7 6.6%

In 9M 2016, Intertrust Luxembourg achieved year-on-year Adjusted revenue growth of 3.7%, driven by increased billable workforce and renegotiation of fixed fee agreements in order to align fees with the current services provided. Growth was lower than expected due to unavailable hours and fewer billable hours due to fewer FTEs than budgeted because of a tight recruitment market. New business from existing clients showed strong growth, specifically PE/VC activity. The number of entities decreased by 2.7% compared to September 2015 due to less incorporations in the market mainly driven by deal flow in the PE and real estate markets. Outflows due to end of life and insourcing were balanced by inflows with similar revenue.

ARPE growth of 6.6% reflects continuous increase in substance requirements and more complex structures leading to higher fees.

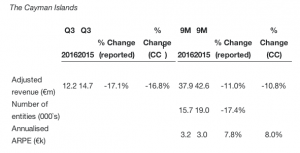

In the Cayman Islands, on a constant currency basis, Adjusted revenue decreased in 9M 2016 by 10.8% driven by a decline in the number of registered office entities as well as the sale of its banking activities in Cayman to Cainvest at the end of 2015, partially offset by higher registered office transfer-out fees.

The re-entry of a competitor in the Cayman Islands led to a reduced inflow and an outflow of 1,554 entities in 9M 2016 (2,898 entities since re-entering the market mid 2015). Remaining outflows in Cayman of 406 entities were driven mainly by end of life and bad debtors. Outflow of Cayman entities in Q3 was almost half of outflow in Q2. Growth in the other businesses, like fiduciary services, fund administration and corporate secretarial services, was less than anticipated. Cayman has had a new MD since September 23rd, with the former MD of Elian Cayman leading the combined teams.

ARPE in constant currency grew by 8% due to outflow of lower ARPE structures, which improves the mix of business.

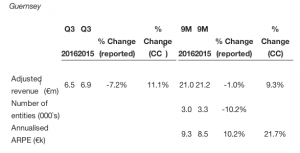

In Guernsey, on a constant currency basis, Intertrust achieved Adjusted revenue growth of 9.3% in 9M 2016. This is driven by additional revenue on FATCA filings and compliance remediation work.

YTD ARPE increased by 21.7% in GBP (10.2% in EUR), driven by the exit of lower margin private client entities from Guernsey and Cayman as well as taking on more complex structures over the last year that generated higher revenue. The decrease in the number of entities was due to an administrative clean-up of 276 entities.

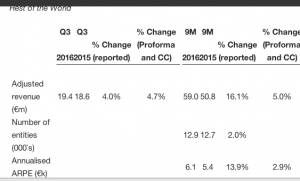

In the Rest of the World (ROW) at constant currency and on a proforma basis, Adjusted revenue grew by 5.0% year on year. The 9M 2016 figures include CorpNordic, acquired in June 2015. On a proforma and constant currency basis, Adjusted revenue growth was driven by strong performance of Spain, Ireland and Singapore, but partially offset by Hong Kong and Switzerland. This growth continues to be driven by increased M&A activity, increased private equity activity and growth in demand from financial institutions.

On a proforma basis, the number of entities remained stable, mainly driven by net inflows in Spain, Ireland, UK, Dubai and Delaware, offset by net outflows in Hong Kong, Curacao and Switzerland. ARPE improved further from €5.4 k in Q3 2015 to €6.1 k in Q3 2016, driven by more complex services resulting in a higher-value service offering to new client entities. The increase in Asian M&A activity is resulting in an increased outbound deal flow from all Asian offices to the network of Intertrust. We also see stronger growth in ROW countries by client wins away from competitors, as a result of a flight to quality.

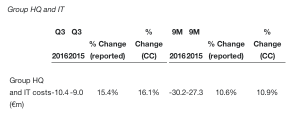

Group HQ and IT costs increased by €2.9 million year-on-year driven by IT costs. The increase mainly comes from IT staff expenses in order to support business and IT initiatives, higher software maintenance costs due to the new applications and higher software amortisation costs due to BAR investments. BAR applications were deployed in most jurisdictions, and this project is completed. Plans to decrease IT latency and down-time are under review, as well as a further strengthening of monitoring and control activities to ensure client data is well-protected.

Financial Calendar

Q3 2016 results – November 3, 2016

Intertrust NV share quotation ex-interim dividend 2016 – November 9, 2016

Record date interim dividend 2016 entitlement – November 10, 2016

Payment date interim dividend 2016 – November 30, 2016

FY 2016 results – February 10, 2017

Publish audited financial statements – April 3, 2017

Q1 2017 results – May 4, 2017

AGM – May 16, 2017

Intertrust NV share quotation ex-final dividend 2016 – May 18, 2017

Record date final dividend 2016 entitlement – May 19, 2017

Payment date final dividend 2016 – June 12, 2017

Investor call

Intertrust CEO David de Buck and CFO Ernesto Traulsen will hold an investor call today at 9:30 a.m. CET to discuss the Company`s 9M 2016 Trading Update. A webcast of the call will be available on the website. Details can be found at http://investors.intertrustgroup.com.

For further information

Intertrust N.V. [email protected]

Anne Louise Metz Tel: +31 20 577 1157

Director of Investor Relations, Marketing & Communications

About Intertrust

Intertrust is the leading global provider of high-value trust and corporate services, with approximately 2,400 employees located throughout a network of 42 offices in 31 jurisdictions across Europe, the Americas, Asia and the Middle-East. The Company focuses on delivering high-quality, tailored services to its clients with a view to building long-term relationships. Intertrust`s business services offering is comprised of corporate services, fund services, capital market services, and private wealth services. Intertrust has leading market positions in selected key geographic markets of its industry, including the Netherlands, Luxembourg, the Cayman Islands and Jersey. Intertrust works with global law firms and accountancy firms, multi-national corporations, financial institutions, fund managers, high net worth individuals and family offices.

For more on this press release including Intertrust N.V. – Consolidated Profit/Loss (unaudited) go to: Intertrust NV Press release – 9M 2016 Results – FINAL at: http://hugin.info/171118/R/2053889/768784.pdf